Forex

Regulation

Explained

- 5-Star Rated Broker Reviews

- Expert Analysis & Insights

- Unmatched Industry Knowledge

- Top 10 Brokers Ranked

Contents

- Overview

- Why Regulation Matters

- Key Global Regulators

- Regulation by Region

- How to Verify a Broker

- 2026 Trends

Trust, Transparency & Safety

Forex regulation isn’t just bureaucracy — it’s the foundation of a safe trading environment. By

choosing regulated brokers and understanding the regulatory landscape, you protect your

investments and contribute to market integrity.

Key Takeaways

- Always verify a broker's regulatory status before opening an account

- Tier-1 regulators offer the strongest investor protection

- Multiple licenses from reputable jurisdictions indicate higher credibility

- Stay informed about regulatory changes that may affect your trading

Discover brokers with verified licenses and strong regulatory oversight

The Global Forex Regulatory Landscape

Forex trading operates within a complex network of international regulatory frameworks.

Understanding these regulations is crucial for protecting your investments and ensuring

you trade with reputable brokers.

120+

Regulatory Bodies

Millions

Protected Traders

Tier-1

Top Jurisdictions

24/7

Market Oversight

What is Forex Regulation?

Forex regulation refers to the rules and oversight mechanisms established by governmental and independent bodies to ensure fair, transparent, and secure trading practices. These regulations govern how brokers operate, how they handle client funds, and what standards they must maintain.

Regulatory bodies classify brokers into different tiers based on the stringency of their requirements. Tier-1 regulators like the FCA (UK), ASIC (Australia), and CFTC (USA) enforce the strictest standards, including capital requirements, regular audits, segregation of client funds, and investor compensation schemes.

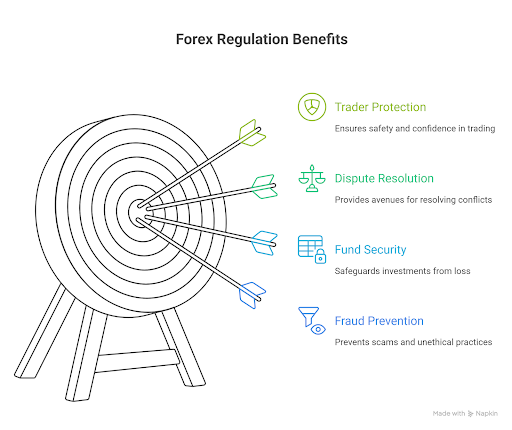

Why Forex Regulation Matters

Regulation is the cornerstone of trust in forex trading. It protects traders, ensures market

integrity, and establishes clear standards for broker operations.

Protection & Transparency

Regulated brokers must segregate client funds, maintain adequate capital reserves, and provide transparent pricing. This framework ensures that your investments are protected even if a broker faces

financial difficulties.

Over 120+ Regulatory Bodies Worldwide

From tier-1 authorities like the FCA and ASIC to regional regulators, the global forex market is overseen by a complex network ensuring fair

trading practices.

Licensing

Ensures brokers meet strict standards

Oversight

Continuous monitoring and compliance

Protection

Safeguards client funds and data

Trust

Builds confidence in the market

Global Regulatory Map

Explore forex regulation by region. Click on each area to discover top regulators, licensing

requirements, and protection standards.

Key Regulators:

- FCA (UK)

- CySEC (Cyprus)

- BaFin (Germany)

Key Regulators:

- ASIC (Australia)

- MAS (Singapore)

- FSA (Japan)

Key Regulators:

- CFTC (USA)

- NFA (USA)

- IIROC (Canada)

Key Regulators:

- MISA (Comoros)

- CMA (Saudi Arabia)

- ISA (Israel)

Key Regulators:

- FSCA (South Africa)

- CMA (Kenya)

- FSC (Mauritius)

Key Regulators:

- CVM (Brazil)

- CNV (Argentina)

- SVS (Chile)

Key Global Regulators

Understand the major regulatory bodies that oversee forex trading worldwide.

FCA

United Kingdom

One of the strictest regulators ensuring segregation of client funds and comprehensive

oversight.

Key Regulators:

- Client Fund Segregation

- £85k FSCS Protection

- Stringent Reporting

ASIC

Australia

Robust regulatory framework with strong enforcement and investor protection measures.

Key Regulators:

- Negative Balance Protection

- Trust Account Requirements

- Regular Audits

CySEC

Cyprus

EU-harmonized regulation with MiFID II compliance and investor compensation scheme.

Key Regulators:

- €20k ICF Protection

- MiFID II Compliant

- Leverage Restrictions

FINMA

Switzerland

Swiss financial regulator known for high standards and banking secrecy protection.

Key Regulators:

- Bank-Level Oversight

- Capital Requirements

- Risk Management

CFTC

United States

Federal agency regulating derivatives markets with strict capital requirements.

Key Regulators:

- $20M Capital Minimum

- Segregated Funds

- NFA Membership

Key Regulators:

- Capital Adequacy Rules

- Business Improvement Orders

- Consumer Protection

Regulations at a Glance

Compare key regulatory features across major jurisdictions

Region

Regulator

Investor Protection

Leverage Cap

Complaint Channel

How to Verify a Broker's License

Follow these simple steps to ensure your broker is properly regulated and licensed.

Find License Number

Locate the broker's regulatory license number on their website, usually in the footer or 'About' section.

Visit Regulator Site

Go to the official website of the regulatory authority (FCA, ASIC, CySEC, etc.).

Check License Status

Use the regulator's search tool to verify the license is active and in good standing.

Compare Details

Ensure the company name and license details match exactly with the broker's information.

Quick Links to Regulator Search Tools

FCA Register

UK

ASIC Connect

Australia

CySEC Search

Cyprus

Multiple Licenses = Higher Credibility

Brokers licensed in multiple tier-1 jurisdictions demonstrate commitment to compliance and offer additional protection.

Beware of Offshore-Only Licenses

Always verify that a broker's license is current and hasn't been suspended or revoked.

Beware of Offshore-Only Licenses

Some jurisdictions have minimal oversight. Prefer brokers with at least one tier-1 or tier-2 license.

Segregated Accounts Matter

Ensure your broker keeps client funds separate from operating capital — it's a key protection mechanism.

2026 Regulatory Trends

The forex regulatory landscape is evolving rapidly. Stay informed about key developments

shaping the industry.

Enhanced MiFID III Proposals

2024

Europe proposes stricter leverage limits and enhanced product intervention powers.

Impact:

Crypto Integration

2024-25

Major regulators clarify frameworks for crypto-forex hybrid products and CFDs.

Impact:

Digital Licensing

2025

Streamlined online application processes and blockchain- based license verification.

Impact:

AI & Algorithmic Trading Oversight

2025+

New regulations for AI-driven trading platforms and automated execution systems.

Impact:

“The future of forex regulation lies in harmonization — creating consistent standards while respecting regional market characteristics.”

— Global Financial Regulatory Expert, 2024

Forex Regulation Explained – The

Complete Global Guide (2026)

Forex regulation refers to the official oversight of brokers and trading platforms by government-authorized financial authorities. These regulatory bodies set strict standards that brokers must follow, including capital requirements, client fund protection, reporting obligations, and fair trading practices. For traders, regulation provides security, transparency, and confidence in the financial markets, helping prevent fraud and ensuring that funds are handled responsibly.

This guide provides a comprehensive look at the world’s major forex regulators, including the FCA (UK), CySEC (Cyprus), ASIC (Australia), NFA (USA), FSCA (South Africa), and other notable authorities. You will also learn how compliance standards differ across regions and get practical steps to verify a broker’s license, ensuring you trade safely with trustworthy platforms.

⚠️ Risk Disclaimer: Trading forex and CFDs carries a high level of risk and may not be suitable for all investors. Losses can exceed deposits. Always trade responsibly and consider your financial situation before engaging in trading activities.

What is Forex Regulation?

Definition and Purpose

Forex regulation is the legal and official oversight of forex brokers and trading platforms by government-authorized or independent financial authorities. Regulatory bodies establish rules and standards that brokers must comply with, including capital adequacy, transparent pricing, segregation of client funds, reporting obligations, and fair trading practices.

The primary goal of forex regulation is to protect traders and maintain the integrity of financial markets. By enforcing strict rules, regulators ensure that brokers operate responsibly, clients’ funds are safeguarded, and market manipulation or unethical practices are minimized.

In essence, regulation serves as a safeguard, giving traders confidence that they are interacting with licensed, accountable, and transparent brokers.

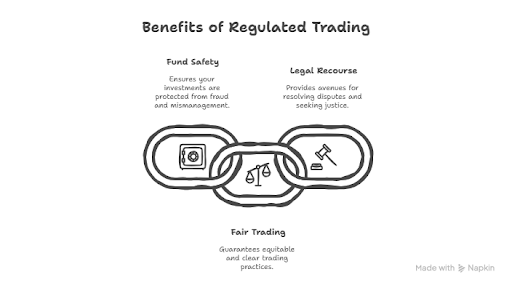

Why Regulation Matters in Forex Trading

Forex regulation isn’t just bureaucratic red tape—it’s the essential framework that protects traders from fraud, ensures their funds remain secure, and provides recourse when disputes arise. Understanding why regulation matters can mean the difference between trading with confidence and losing your entire investment to an unscrupulous broker.

The Three Pillars of Forex Regulation

1. Fraud Prevention

Regulated brokers must undergo rigorous vetting before receiving their licenses. They’re required to maintain transparent business practices, provide accurate marketing materials, and avoid deceptive tactics. Regulators actively monitor brokers for signs of fraudulent activity, including price manipulation, misleading claims about returns, and unauthorized trading on client accounts.

Without regulation, fraudulent brokers can operate with impunity, using sophisticated marketing to lure unsuspecting traders into scams that include Ponzi schemes, signal seller fraud, and outright theft of deposits.

2. Fund Security

Perhaps the most critical protection regulation provides is segregation of client funds. Regulated brokers must keep client money separate from operational funds in segregated bank accounts. This means if a broker goes bankrupt, your trading capital isn’t used to pay creditors or operational expenses.

Additionally, many regulatory jurisdictions offer compensation schemes. For example, the UK’s Financial Services Compensation Scheme (FSCS) can cover up to £85,000 per person if an FCA-regulated broker fails. The Cyprus Investor Compensation Fund (ICF) provides up to €20,000 in coverage.

3. Dispute Resolution

When conflicts arise between traders and brokers, regulation provides structured mechanisms for resolution. Regulated brokers must have formal complaint procedures, and if internal resolution fails, traders can escalate issues to financial ombudsman services or regulatory bodies that have enforcement powers.

Unregulated brokers have no obligation to respond to complaints, leaving traders with essentially no recourse beyond expensive and uncertain legal action.

Real-World Examples: When Regulation Works (and When It's Absent)

Example 1: FXCM's $7 Million Fine and Swiss Franc Crisis (2017)

The Scandal: The U.S. Commodity Futures Trading Commission (CFTC) fined FXCM, once one of the world’s largest retail forex brokers, $7 million for engaging in deceptive practices. FXCM had claimed to offer “No Dealing Desk” execution, suggesting they simply matched client orders without conflicts of interest. However, investigations revealed they were routing trades to a related market maker from which they received substantial payments—essentially profiting when clients lost.

The Regulatory Response: The CFTC discovered these violations during investigations following the 2015 Swiss Franc crisis, when FXCM suffered massive losses and required a $300 million bailout. U.S. regulators ultimately revoked FXCM’s registration, forcing them to exit the U.S. market entirely.

Why It Matters: This case demonstrates how major regulators like the CFTC actively investigate broker practices and have real enforcement power. Without this regulatory oversight, FXCM’s deceptive practices would have continued indefinitely, costing traders millions through conflicts of interest they didn’t know existed.

Example 2: Refco Collapse (2005)

The Scandal: Refco was a major U.S. futures and forex broker that collapsed spectacularly in 2005 when it emerged that CEO Phillip Bennett had hidden $430 million in bad debts through fraudulent transactions. The company went from being valued at $3.5 billion to bankruptcy in less than a week.

The Regulatory Response: Because Refco was regulated by the CFTC and NFA, client funds were segregated according to strict regulatory requirements. When the company collapsed, customer accounts were transferred to other brokers, and the vast majority of clients recovered their funds intact. The CFTC’s segregation rules meant Refco couldn’t use client money to cover corporate debts.

Why It Matters: This case perfectly illustrates the value of fund segregation requirements. Despite massive corporate fraud, traders’ capital was protected. Had Refco been unregulated, clients would have been unsecured creditors waiting years to recover pennies on the dollar—if anything at all.

Example 3: Alpari UK Insolvency (2015)

The Scandal: While not a scandal in the traditional sense, Alpari UK’s sudden insolvency following the Swiss National Bank’s unexpected currency peg removal in January 2015 demonstrates both the risks in forex trading and the protections regulation provides.

When the Swiss Franc surged 30% in minutes, many brokers faced massive losses as clients’ positions went deeply negative faster than stop-losses could execute. Alpari UK, an FCA-regulated broker, couldn’t absorb these losses and entered insolvency.

The Regulatory Response: Because Alpari UK was FCA-regulated, the Financial Services Compensation Scheme (FSCS) stepped in. Eligible clients received compensation up to £50,000 (the limit at that time), and the orderly insolvency process ensured proper handling of client accounts.

Why It Matters: This case shows that even legitimate, regulated brokers can fail due to extraordinary market conditions. However, regulation provided a safety net through compensation schemes and orderly wind-down procedures. Traders with unregulated brokers facing similar circumstances would have had no protection whatsoever.

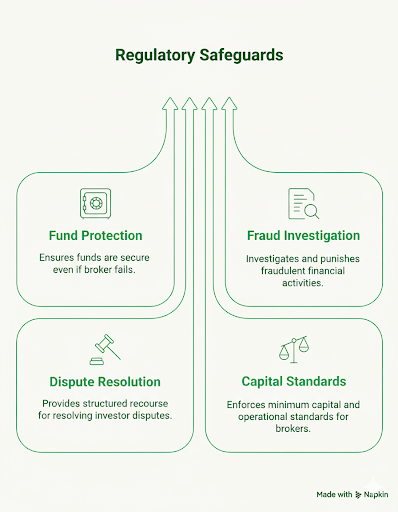

Strong regulation from bodies like the FCA (UK), CFTC/NFA (US), ASIC (Australia), or CySEC (Cyprus) ensures that:

- Your funds are protected even if your broker fails

- Fraudulent practices are investigated and punished

- You have structured recourse when disputes arise

- Brokers maintain minimum capital requirements and operational standards

While regulated brokers may have slightly higher costs or more restrictive leverage limits, these trade-offs are minimal compared to the existential risk of trading with unregulated entities where your entire investment exists purely on trust—with no safety net when that trust is violated.

How Forex Regulation Works Worldwide

The global forex market operates 24 hours a day across multiple jurisdictions, creating a complex regulatory landscape where brokers can choose their domicile and traders must navigate varying levels of protection. Understanding how different regulators operate and what standards they enforce is crucial for making informed decisions about where to trade.

Categories of Regulators

Not all forex regulators are created equal. The jurisdiction where a broker is licensed significantly impacts the level of protection you receive, the trading conditions available, and your recourse options if problems arise.

Major Regulators (Tier 1)

These are the gold standard of forex regulation, offering the strongest protections and most rigorous oversight:

Financial Conduct Authority (FCA) - United Kingdom

The FCA is widely considered the world’s strictest forex regulator. UK-authorized brokers must maintain substantial capital reserves, segregate client funds in top-tier banks, and comply with comprehensive conduct rules. The FCA conducts regular audits and has powerful enforcement capabilities, including the ability to freeze assets and ban individuals from financial services. Traders benefit from up to £85,000 protection through the Financial Services Compensation Scheme (FSCS).

The FCA’s rigorous approach means fewer brokers qualify for authorization—which is precisely why an FCA license carries such weight. Leverage for retail clients is capped at 30:1 for major currency pairs under European Securities and Markets Authority (ESMA) rules that the UK maintained post-Brexit.

Commodity Futures Trading Commission (CFTC) & National Futures Association (NFA) - United States

The U.S. operates a dual regulatory system where the CFTC sets policy and enforces regulations while the NFA handles day-to-day oversight of member firms. U.S. regulation is exceptionally strict: brokers must maintain a minimum capital of $20 million (far higher than most jurisdictions), report detailed financial information monthly, and comply with strict anti-fraud rules.

American traders face the most restrictive trading conditions globally—leverage is capped at 50:1 for major pairs, and FIFO (first-in-first-out) rules restrict trading strategies. However, these restrictions come with ironclad protections. U.S.-registered forex brokers have never had a client fund failure resulting in losses.

Australian Securities and Investments Commission (ASIC) - Australia

ASIC has evolved into one of the world’s most respected regulators, striking a balance between trader protection and market accessibility. Brokers must hold an Australian Financial Services License (AFSL), maintain minimum capital of AUD $1 million, and segregate client funds with approved Australian banks.

Following regulatory reforms in 2021, ASIC implemented leverage restrictions (30:1 for major pairs) and negative balance protection for retail clients. The regulator actively monitors broker compliance through regular audits and has demonstrated willingness to take enforcement action, including banning brokers that violate consumer protection standards.

Cyprus Securities and Exchange Commission (CySEC) - Cyprus

As a European Union member, CySEC-regulated brokers must comply with the Markets in Financial Instruments Directive (MiFID II), allowing them to “passport” their services throughout the European Economic Area. This makes Cyprus a popular jurisdiction for brokers serving European clients.

CySEC requires €730,000 minimum capital, client fund segregation, and participation in the Investor Compensation Fund (ICF), which provides up to €20,000 coverage per client. While historically viewed as less stringent than the FCA or ASIC, CySEC has significantly strengthened oversight in recent years following EU-wide regulatory harmonization.

The regulator conducts on-site inspections and has revoked licenses of brokers violating rules, though enforcement has sometimes been criticized as reactive rather than proactive.

Financial Sector Conduct Authority (FSCA) - South Africa

| Tier | Regulator | Jurisdiction | Min. Capital Requirement | Max. Leverage | Segregation Required | Compensation Scheme | Enforcement Strength | Key Characteristics |

| TIER 1 | FCA | United Kingdom | £730,000 (~$920,000) | 30:1 | Yes (strict) | Up to £85,000 (FSCS) | Very Strong | Gold standard regulation; rigorous audits; powerful enforcement; maintained ESMA rules post-Brexit |

| TIER 1 | CFTC/NFA | United States | $20,000,000 | 50:1 | Yes (strict) | No (but zero client fund failures) | Very Strong | Highest capital requirements globally; monthly reporting; FIFO rules; most restrictive conditions but strongest protections |

| TIER 1 | ASIC | Australia | AUD $1,000,000 (~$650,000) | 30:1 | Yes (strict) | No compensation scheme | Strong | Balanced approach; 2021 reforms added leverage caps and negative balance protection; active enforcement |

| TIER 1 | CySEC | Cyprus (EU) | €730,000 (~$800,000) | 30:1 | Yes (MiFID II) | Up to €20,000 (ICF) | Moderate-Strong | EU passporting rights; MiFID II compliance; improved significantly in recent years; on-site inspections |

| TIER 1 | FSCA | South Africa | Varies (substantial) | 25:1 | Yes | No compensation scheme | Strong | Leading African regulator; comparable to other Tier 1; 2023 leverage restrictions; public enforcement register |

Secondary Regulators (Tier 2)

These regulators maintain solid standards and provide meaningful protection, though typically with less stringent requirements than Tier 1 jurisdictions:

Monetary Authority of Singapore (MAS) - Singapore

MAS is highly respected in Asia and maintains rigorous standards for financial services. However, it primarily regulates institutional forex trading. Most retail forex brokers in Singapore operate under a less comprehensive Capital Markets Services (CMS) license rather than full banking licenses. MAS requires substantial capital reserves and regular reporting but has less prescriptive rules around retail forex marketing and leverage than some Tier 1 regulators.

Federal Financial Supervisory Authority (BaFin) - Germany

BaFin is one of Europe’s most respected financial regulators, overseeing banks, insurance companies, and investment firms. German brokers must comply with both national regulations and EU directives (MiFID II). BaFin is known for conservative oversight and strong enforcement, though relatively few forex brokers choose German licensing due to stringent requirements and operational costs.

Financial Services Agency (FSA) - Japan

Japan’s FSA regulates the world’s third-largest forex market by volume. Japanese regulations are notably strict on leverage (25:1 maximum, among the lowest globally) and require substantial capital reserves. The FSA maintains a comprehensive licensing system and has strong enforcement powers, regularly penalizing brokers for violations.

However, Japanese regulation focuses heavily on domestic brokers serving Japanese residents. Many international brokers don’t seek FSA licensing due to unique regulatory requirements specific to the Japanese market.

Swiss Financial Market Supervisory Authority (FINMA) - Switzerland

FINMA regulates Switzerland’s financial sector with standards comparable to Tier 1 jurisdictions. However, FINMA primarily oversees banks and large financial institutions. Most retail forex brokers don’t qualify for full Swiss banking licenses and instead operate under less comprehensive registration schemes or seek licensing in other jurisdictions while maintaining Swiss business operations.

| TIER 2 | MAS | Singapore | Substantial | 20:1 (guidelines) | Yes | Limited | Strong | Primarily institutional focus; respected in Asia; less prescriptive for retail forex |

| TIER 2 | BaFin | Germany (EU) | €730,000 (MiFID II) | 30:1 | Yes (MiFID II) | EU schemes apply | Very Strong | Conservative oversight; few retail forex brokers due to stringent requirements; strong enforcement |

| TIER 2 | FSA | Japan | Substantial | 25:1 | Yes | Yes | Strong | Third-largest forex market; strict regulations; focuses on domestic brokers; unique market requirements |

| TIER 2 | FINMA | Switzerland | Very High (banking) | Varies | Yes | Yes (for banks) | Very Strong | Primarily banks/large institutions; most retail brokers don’t qualify for full licensing |

Offshore Regulators (Tier 3)

These jurisdictions offer easier licensing requirements, lower costs, and minimal operational restrictions—making them attractive to brokers but offering significantly less protection to traders:

Vanuatu Financial Services Commission (VFSC) - Vanuatu

Vanuatu has become one of the most popular offshore licensing jurisdictions. The VFSC offers relatively straightforward licensing with minimal capital requirements (often as low as $50,000), no segregation mandates, and light regulatory oversight. Brokers favor Vanuatu because they can offer high leverage (often 1000:1 or higher) without operational restrictions.

However, the VFSC provides minimal consumer protection. There’s no compensation scheme, limited enforcement capability, and recourse options are essentially non-existent if disputes arise. The regulator conducts few on-site inspections and relies heavily on self-reporting by brokers.

International Financial Services Commission (IFSC) - Belize

Belize offers low-cost, accessible licensing that many brokers use for international clients they can’t serve under stricter regulations. Capital requirements are minimal (typically $50,000), and operational oversight is light. While the IFSC requires some basic compliance measures, enforcement is limited and there’s no meaningful compensation scheme for traders.

Financial Services Authority (FSA) - Seychelles

The Seychelles FSA has become increasingly popular among forex and CFD brokers in recent years. Licensing requirements are moderate—higher than Vanuatu but lower than Tier 1 jurisdictions—with capital requirements around $50,000. The FSA requires some operational standards and segregation of client funds, positioning itself as a middle-ground between pure offshore jurisdictions and major regulators.

However, enforcement capability remains limited, compensation schemes are absent, and the jurisdiction’s small size and limited resources mean oversight is less comprehensive than major regulators provide.

| TIER 3 | VFSC | Vanuatu | ~$50,000 | 500:1-1000:1+ | No | No | Very Weak | Popular offshore jurisdiction; minimal oversight; no compensation; very high leverage allowed; limited enforcement |

| TIER 3 | IFSC | Belize | ~$50,000 | 500:1+ | Minimal | No | Weak | Low-cost licensing; light oversight; no meaningful compensation; limited enforcement capability |

| TIER 3 | FSA | Seychelles | ~$50,000 | 500:1+ | Some requirements | No | Weak | Middle-ground offshore; moderate standards; limited enforcement; no compensation scheme |

Emerging Market Regulators

Developing economies are increasingly establishing forex regulatory frameworks, though maturity and enforcement capability vary significantly:

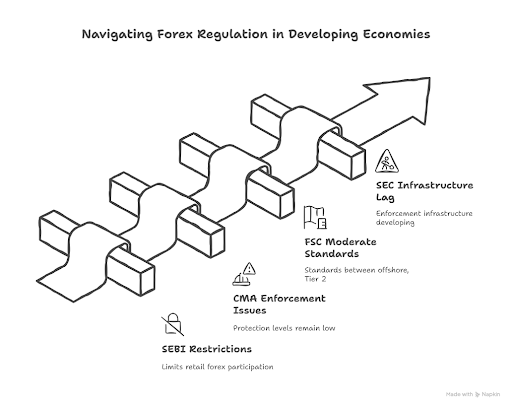

Securities and Exchange Board of India (SEBI) has created regulations for currency derivatives but maintains strict controls on forex trading, limiting retail participation to exchange-traded instruments rather than OTC spot forex.

Capital Markets Authority (CMA) – Kenya regulates forex brokers serving Kenyan clients, requiring local licensing and establishing standards for capital adequacy and conduct. However, enforcement challenges and limited resources mean protection levels remain below Tier 1 standards.

Financial Services Commission (FSC) – Mauritius offers an emerging regulatory framework that some brokers use to serve African markets, with moderate standards positioned between offshore and Tier 2 jurisdictions.

Securities and Exchange Commission (SEC) – Nigeria has established regulations for forex trading, requiring brokers to obtain authorization and meet capital requirements, though enforcement infrastructure is still developing.

The Mwali International Services Authority (MISA) is an offshore financial regulator based on Mwali (Mohéli), an island within the Union of the Comoros. MISA issues offshore financial licenses and facilitates the registration of international businesses, including forex brokers, insurance companies, and gambling firms.

The challenge with emerging market regulators is inconsistency. Regulatory frameworks may exist on paper, but implementation, enforcement, and dispute resolution mechanisms often lag behind established jurisdictions.

Regulatory Principles

Despite jurisdictional differences, effective forex regulation rests on common principles that protect traders and maintain market integrity:

Licensing Requirements

Legitimate regulators implement comprehensive licensing processes that vet broker ownership, management, business plans, and financial stability before authorization. This isn’t a rubber-stamp process—major regulators regularly reject applications from inadequately capitalized or poorly structured firms.

Application Process: Tier 1 regulators require detailed applications including company structure, ownership information, business plans, compliance procedures, risk management frameworks, and evidence of adequate capital. Background checks on directors and key personnel are standard, with individuals having criminal records or regulatory violations typically disqualified.

Ongoing Obligations: Licensing isn’t permanent. Brokers must renew authorization regularly, demonstrate continued compliance with evolving regulations, and notify regulators of material business changes. The FCA, for example, can withdraw authorization if firms fail to maintain standards or deceive clients.

Public Registers: Credible regulators maintain public databases where anyone can verify a broker’s license status, authorized activities, and regulatory history. Before opening an account, checking the regulator’s official register—not just trusting information on the broker’s website—is essential due diligence.

Capital Adequacy and Leverage Limits

Capital adequacy requirements ensure brokers can withstand normal business volatility and meet obligations to clients even during market stress.

Minimum Capital Requirements: These vary dramatically by jurisdiction. The CFTC requires $20 million for U.S. brokers, while the FCA mandates €730,000 for most forex firms. ASIC requires AUD $1 million, whereas offshore jurisdictions like Vanuatu may require only $50,000. Higher capital requirements mean brokers have greater financial cushion to absorb losses and protect client funds.

Ongoing Capital Monitoring: Regulators don’t just check capital at licensing—they require regular reporting to ensure brokers maintain adequate financial resources. The FCA uses a “three-dimensional” approach examining capital resources, liquidity, and concentration risk to assess whether firms remain viable.

Leverage Restrictions: Following the 2008 financial crisis and subsequent retail trading disasters, major regulators have implemented leverage caps to limit retail trader exposure to catastrophic losses:

- European regulators (ESMA framework): 30:1 for major currency pairs, 20:1 for minor pairs, 10:1 for commodities, 5:1 for individual stocks, 2:1 for cryptocurrencies

- FCA (UK): Maintained ESMA limits post-Brexit

- CFTC/NFA (US): 50:1 for major pairs, 20:1 for minor pairs

- ASIC (Australia): 30:1 for major pairs following 2021 reforms

- FSCA (South Africa): 25:1 for retail clients

These restrictions are controversial—traders often complain they limit profit potential and flexibility. However, regulators implemented them after extensive data showing that higher leverage strongly correlates with faster account depletion and greater losses for retail traders.

Offshore jurisdictions offering 500:1 or 1000:1 leverage aren’t providing advantages—they’re facilitating substantially higher risk with no corresponding increase in profit probability.

| Principle | Tier 1 Implementation | Tier 2 Implementation | Tier 3 (Offshore) Implementation |

| Licensing Requirements | Comprehensive vetting; background checks; detailed business plans; can reject applications | Moderate vetting; established procedures; some may be less stringent | Minimal vetting; easy approval; self-reporting focused |

| Capital Adequacy | $650K-$20M minimum; ongoing monitoring; stress testing | Moderate requirements; regular reporting | $50K typical; limited monitoring |

| Leverage Limits | 25:1 to 50:1 maximum | 20:1 to 30:1 typical | 500:1 to 1000:1+ (unrestricted) |

| Fund Segregation | Mandatory; top-tier banks; frequent reconciliation; external audits | Required; regular monitoring | Not required or minimally enforced |

| Compensation Schemes | Often available (£20K-£85K) | Sometimes available | None |

| Reporting Frequency | Monthly or quarterly; detailed | Quarterly; moderate detail | Annual or minimal |

| Independent Audits | Annual; strict requirements; direct regulator reporting | Annual; standard requirements | Limited or self-selected |

| On-site Examinations | Regular and unannounced | Periodic | Rare or never |

| Enforcement Powers | Strong; fines to license revocation; proven track record | Moderate; established procedures | Weak; limited resources and authority |

Client Fund Segregation

Segregation of client funds from broker operational capital is perhaps the single most important protection regulation provides.

Segregated Accounts: Regulated brokers must hold client deposits in segregated bank accounts separate from company funds. This means client money isn’t used to pay rent, salaries, or other operational expenses—and crucially, if the broker goes bankrupt, client funds aren’t available to creditors.

Major regulators specify which banks can hold client funds (typically requiring stable, highly-rated institutions), how frequently reconciliations must occur, and detailed record-keeping requirements to track client money precisely.

Trust Account Structures: Some jurisdictions require brokers to hold client funds in trust, creating even stronger legal separation. Funds held in trust legally belong to clients, not the broker, providing additional protection in insolvency scenarios.

Segregation Verification: Reputable regulators require external auditors to verify segregation annually and report findings directly to the regulatory authority. The FCA goes further, requiring client money audits more frequently and mandating that brokers have detailed client money resolution packs ready if the firm fails—essentially a roadmap for returning funds quickly.

The Problem with Unregulated Brokers: Brokers without meaningful regulatory oversight have zero obligation to segregate funds. Your deposit goes into the general company account alongside all other money, making you an unsecured creditor if the broker fails. Recovery in such circumstances is unlikely and would require expensive international legal action with minimal success probability.

Reporting and Audits

Transparency through reporting and independent audits ensures regulators can monitor broker health and identify problems before they become crises.

Financial Reporting: Major regulators require detailed monthly or quarterly financial statements showing capital positions, client money holdings, revenue sources, and risk exposures. The CFTC requires monthly reporting within 17 business days of month-end, while the FCA requires quarterly returns with additional annual audited accounts.

Client Money Reporting: Beyond general financial reporting, regulators require specific reporting on client fund segregation. This includes daily reconciliations of client money positions, immediate notification if segregation requirements are breached, and detailed tracking of money flows between client and house accounts.

Independent Audits: Annual audits by qualified external auditors are standard requirements. Auditors must verify financial statements, test segregation controls, review risk management procedures, and report findings to both the broker and regulator. Critically, auditors have obligations to report directly to regulators if they identify serious concerns—they can’t simply resign quietly.

On-site Examinations: Proactive regulators conduct periodic on-site examinations beyond reviewing reported data. The CFTC, FCA, and ASIC regularly visit broker offices unannounced to inspect records, interview staff, and verify that actual practices match reported procedures.

Enforcement and Penalties: When audits or examinations reveal violations, strong regulators have graduated enforcement tools:

- Warning letters for minor infractions

- Fines for more serious violations (ranging from thousands to millions)

- Operational restrictions limiting new business until issues are resolved

- License suspension preventing client acquisition but allowing orderly wind-down

- License revocation forcing business closure

The existence of meaningful enforcement powers—and willingness to use them—separates genuine regulators from registration schemes that exist primarily to create the appearance of oversight without substance.

Impact of Regulation on Traders

Forex regulation is not just a formality — it defines how secure, transparent, and fair your trading environment is. When you trade with a regulated broker, you’re protected by a legal framework designed to ensure that your funds are safe, your trades are executed fairly, and that you have avenues for redress if anything goes wrong.

Let’s explore the main ways regulation directly impacts traders worldwide.

Security of Funds

1. Segregated Accounts – The Foundation of Financial Safety

Regulated brokers are required to hold client funds in segregated accounts, separate from their company’s operational accounts. This ensures that your deposits aren’t used for the broker’s expenses, investments, or hedging activities. If the broker experiences financial trouble or bankruptcy, your funds remain untouched.

For example:

- FCA and CySEC demand that brokers keep client money in Tier-1 banks (large, stable financial institutions).

- These funds must also be reconciled daily, ensuring every cent of client capital matches actual bank balances.

This simple but strict rule protects traders from one of the biggest risks in the forex industry — the misuse or commingling of client money.

2. Compensation Schemes – Last-Resort Protection

Some of the world’s top regulators also provide compensation mechanisms in case a broker goes bankrupt or fails to return client funds:

- UK – FSCS (Financial Services Compensation Scheme): Covers up to £85,000 per trader if a broker regulated by the FCA becomes insolvent.

- Cyprus – ICF (Investor Compensation Fund): Provides compensation of up to €20,000 per eligible client.

- EU (MiFID II): Requires EU member states to maintain national compensation schemes to protect retail investors.

- Japan – FSA: Mandates strict fund protection but relies on broker-held investor protection reserves rather than a centralized scheme.

These mechanisms serve as the final safety net for traders, ensuring that even in worst-case scenarios, investors recover at least a portion of their capital.

3. Practical Implications for Traders

- Always check that your broker states where client funds are held and whether segregation policies are audited.

- Avoid brokers that keep all funds in-house or offer “custodian services” without third-party verification.

- Confirm participation in a recognized compensation scheme.

Real-World Example:

n 2015, Alpari UK collapsed after the Swiss National Bank unpegged the CHF from the Euro. Clients regulated under the FCA received compensation through the FSCS, protecting tens of thousands of retail traders who might otherwise have lost their deposits.

Trading Restrictions

Regulators enforce strict rules around leverage, margin requirements, and product offerings to protect traders from catastrophic losses.

1. Leverage Limits – Reducing Risk Exposure

High leverage can amplify profits — but also losses. To protect retail traders from excessive exposure, regulators cap maximum leverage:

- FCA / ESMA (EU):

- 30:1 for major FX pairs

- 20:1 for minors

- 10:1 for commodities

- 2:1 for cryptocurrencies

- ASIC (Australia): Mirrors ESMA rules, 30:1 for majors.

- NFA / CFTC (US): 50:1 for major pairs, 20:1 for minors.

- FSCA (South Africa): Typically aligns with ASIC and ESMA levels.

By contrast, offshore brokers often advertise 500:1 or even 1000:1 leverage — appealing but extremely dangerous, especially for new traders.

2. Margin Requirements and Stop-Out Rules

Regulated brokers must clearly outline:

- Initial margin (minimum deposit required to open a trade).

- Maintenance margin (minimum equity needed to keep trades open).

- Stop-out levels (when positions are automatically closed to prevent negative balances).

This ensures transparency and prevents the “margin call traps” common in unregulated environments.

3. Negative Balance Protection

In top-tier jurisdictions (UK, EU, Australia), negative balance protection (NBP) is mandatory.

This means traders cannot lose more than they deposit, even in highly volatile market events like the 2015 CHF shock or the 2020 oil price collapse.

4. Product Offering Restrictions

Regulators may also restrict certain high-risk instruments:

- Binary options are banned in the UK and EU.

- Cryptocurrency CFDs are limited to experienced investors.

These rules safeguard retail clients from complex, high-volatility products that can cause rapid losses.

Real-World Example

Following the ESMA intervention in 2018, thousands of European traders benefited from negative balance protection and reduced leverage exposure — dramatically lowering retail loss ratios across the EU.

Dispute Resolution

Even with strong rules in place, disputes can occur — from withdrawal issues to execution errors or slippage disputes. Regulation provides clear, transparent systems for resolution.

1. Internal Complaint Handling

Every regulated broker must implement an internal complaint policy that:

- Acknowledges customer complaints within a set period (usually 5–10 business days).

- Investigates and provides a formal response (often within 8 weeks under FCA rules).

- Maintains detailed complaint records available to the regulator on request.

This ensures that traders’ issues are formally addressed rather than ignored or delayed.

2. External Mediation or Regulator Escalation

If a broker fails to resolve the issue satisfactorily, traders can escalate complaints to:

- UK: Financial Ombudsman Service (FOS) – Free, impartial dispute resolution for FCA-regulated firms.

- Cyprus: CySEC’s Investor Compensation Fund Committee.

- Australia: Australian Financial Complaints Authority (AFCA).

US: NFA’s arbitration process, which can impose fines or revoke broker membership.

3. Transparency and Accountability

Regulators frequently publish disciplinary actions, fines, or license suspensions, allowing traders to verify a broker’s compliance record. For instance:

- CySEC publishes monthly enforcement reports.

- The NFA’s BASIC system allows traders to see every disciplinary action a broker has faced.

4. Real-World Case Study: FXCM (2017)

In 2017, the U.S. NFA and CFTC fined FXCM $7 million and permanently banned it from operating in the U.S. after discovering it had misled clients about order execution practices.

While this hurt the brand, it demonstrated how effective regulation protects retail investors and enforces market integrity.

Conclusion

In the fast-paced world of forex trading, regulation isn’t just a box to tick…

It’s your first and strongest layer of protection. It defines whether your trading experience will be transparent, fair, and secure, or vulnerable to manipulation and risk.

By understanding how global regulators like the FCA, ASIC, CySEC, NFA, and FSCA operate, traders can make smarter, safer choices. Regulation ensures that brokers safeguard your funds, offer realistic leverage, maintain transparent pricing, and handle disputes fairly.

Choosing a regulated broker means choosing accountability — a company that answers not only to its clients but also to recognized financial authorities. It’s the difference between trading in a secure environment versus stepping into a market where anything goes.

While the lure of high leverage and lenient offshore rules may seem appealing, unregulated brokers come with real risks: frozen accounts, hidden fees, or worse — the loss of your capital with no recourse.

To protect yourself:

- Always verify broker licenses on official regulatory websites.

- Understand the protections your jurisdiction offers, such as compensation schemes and negative balance protection.

- Stay updated with regulatory news and enforcement actions, as they often signal changes in market integrity.

Ultimately, regulation builds trust, and trust is the foundation of sustainable trading. Whether you’re a beginner or a seasoned trader, knowing who oversees your broker — and how — is as important as knowing how to read a chart.

FAQs

How do I check if a broker is regulated?

Visit the broker’s website and locate their regulatory license number (usually in the footer). Then, go to the regulator’s official website and use their search tool to verify the license is active. Always cross-check the company name and registration details match exactly.

What's the difference between Tier-1 and Tier-3 regulation?

Regulation tiers generally refer to the jurisdiction’s credibility and strictness:

- Tier-1: Highly respected regulators like the FCA (UK), ASIC (Australia), or CFTC/NFA (USA). They enforce strict capital requirements, client fund segregation, and robust reporting standards. Brokers regulated here are considered very trustworthy.

- Tier-3: Less strict regulators, often in offshore jurisdictions like Vanuatu, Belize, or Saint Vincent & the Grenadines. They have fewer requirements, lower oversight, and less investor protection. While trading with Tier-3 brokers is legal, the risks are higher.

Is offshore trading legal?

Yes, trading with offshore brokers is legal in most countries, but:

- Local laws apply: Some countries restrict or prohibit trading with offshore brokers. Always check your local regulations.

- Risk considerations: Offshore brokers may offer higher leverage or lower fees but often lack investor protection and may have weaker dispute resolution mechanisms.

Can a broker lose their license?

Yes, brokers can lose their license if they:

- Fail to comply with regulatory standards

- Mismanage client funds

- Engage in fraudulent or unethical practices

Regulators may suspend, revoke, or fine brokers depending on the severity of violations.

Do all regulated brokers offer compensation?

No. Compensation schemes vary by regulator:

- Some regulators, like the FCA (UK), have investor protection schemes that can cover clients up to a certain amount if the broker goes bankrupt.

- Other regulators may not offer compensation, but they usually enforce fund segregation to protect client money. Always check the broker’s regulatory framework to understand what protections exist.

What are the leverage limits for retail traders?

Leverage limits depend on the regulator and the type of trader:

- Europe (ESMA): Max leverage 1:30 for major currency pairs, 1:20 for minors, 1:2 for cryptocurrencies.

- UK (FCA): Similar ESMA rules apply.

- Australia (ASIC): Up to 1:30 for majors for retail clients.

- Offshore brokers: Leverage can go as high as 1:500 or more, but higher leverage increases risk significantly.

Are forex brokers regulated?

Not all forex brokers are regulated. Regulated brokers operate under the supervision of financial authorities to ensure they meet strict standards for client protection, capital requirements, and transparent trading practices. Examples of well-known regulators include the FCA (UK), ASIC (Australia), CySEC (Cyprus), and NFA/CFTC (USA).